we are committed to innovation

Explore More Scroll down

Our services help you achieve success

What We Offer

Our professional experts understand the challenges that organisations face today. We address all your business needs on a global scale with integrated solutions for auditing, consultancy, corporate finance services and legal advice, ensuring that your business receives the strategic and operational support it requires in order to achieve success

Legal

Specialising in law with a strategic focus, oriented towards business needs.

Legal

Specialising in law with a strategic focus, oriented towards business needs.

Consulting

One-stop solutions that add value to your business

Consulting

One-stop solutions that add value to your business

Corporate

We assist companies with financial advice and corporate transactions.

Corporate

We assist companies with financial advice and corporate transactions.

Solutions tailored to your needs

WHAT WE PROVIDE

We understand that each type of professional and each area of a business has its own unique features and challenges that require specialised tailored solutions. A team of experts from each Auren division has developed comprehensive solutions aimed at addressing these specific needs.

We provide you with a genuine All-in-one solutions to support you with the particular challenges of your area of expertise.

CHOOSE YOUR DEPARTMENT

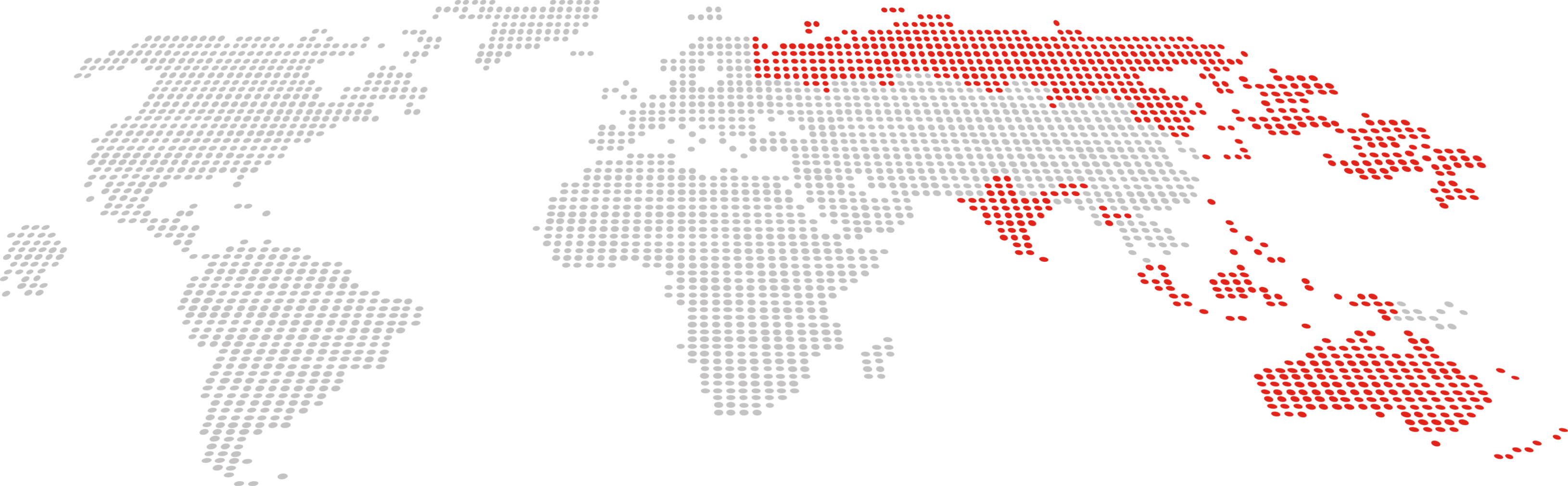

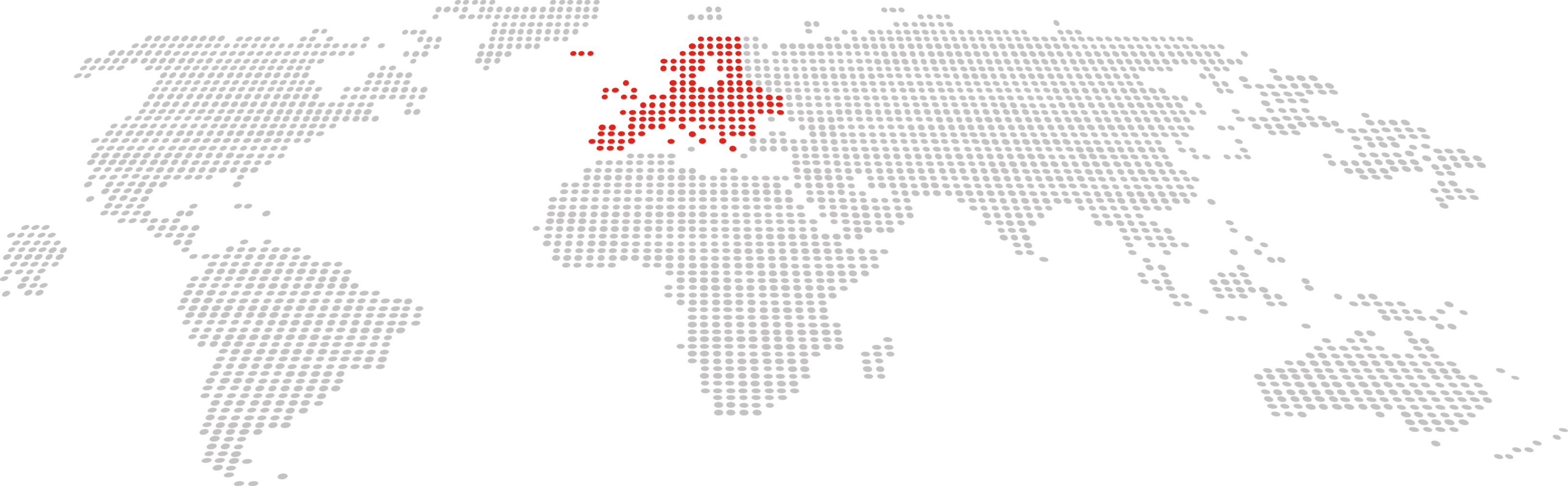

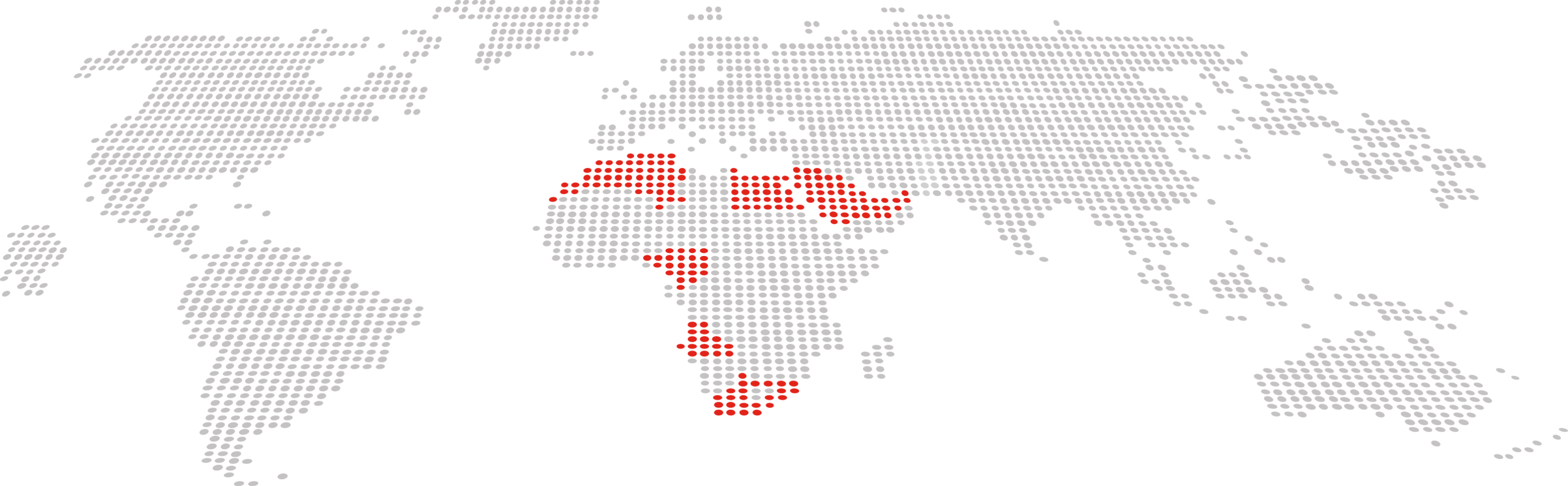

OUR GLOBAL LOCATIONS

Auren is present in 11 countries and operates in 62 offices worldwide. Being a member of the Forum of Firms, led by the Transnational Audit Committee of IFAC (International Federation of Accountants), ensures that we adhere to the highest quality standards.

You can trust in us to provide tailored solutions and expert guidance, customised to your needs, no matter where in the world you are located.

70+ countries

Who We Are?

We are a global multidisciplinary professional services firm devoted to creating value and promoting sustainable development for businesses, individuals and society as a whole.

We always work closely with you and are committed to providing you with quality solutions in auditing, legal advice, consultancy and corporate finance services. Our adaptability and availability are an integral part of our identity.

We guarantee you the pursuit of excellence through the professionalism and experience of our teams, by applying a rigorous and effective work method based on a philosophy that prioritises taking care of our teams and clients.

- .000 clients of every type

- .263 professionals

- offices

LATEST NEWS

Stay up to date with our latest news and insights from our experts. We provide you with valuable content that keeps you informed about market trends, news and advances in auditing services, corporate finance matters, consultancy, tax and legal advice.